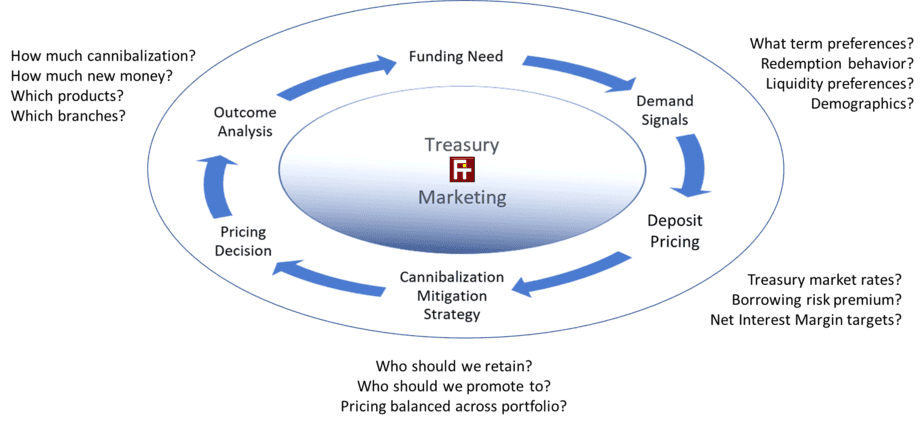

Active Deposit Management Analytics Enabling Active Deposit Management for Credit Unions and Banks Active Deposit Management (ADM) results in Credit Unions and Community BanksImproving pricing discipline and margins by 10-15bpsDetecting and reacting to demand signals Validating key pricing and promotion decisions Increasing lending profitability Working with Industry Leaders What Clients Are Saying A number of SVPs came up to me asking about the extent of FlowTracker capabilities. I will be discussing… at the upcoming Deposit Committee meeting. We were speaking with [a large CU] today and shared the benefits we have seen from FlowTracker as part of our deposit practice … very interested. FlowTracker reports are getting great exposure and attention here. Thank you for providing the guidance to build actionable responses to Pricing and Credit Risk Committee inquiries. The views were well received. As always, we appreciate your support. This Month Our Clients Analyzed 1000 Individual Consumers 1000 Deposit & Loan Accounts DEPOSIT EDGE = Patented Analytics + Expert Advice, Training & Support Learn about DEPOSIT EDGE Contact Us